A couple earning $500,000 a year should feel rich, right? That’s top 2% territory in America—plenty of cash to save, invest, and splurge on the finer things in life. Or so you’d think. But when I dive into the financial lives of high-income households, the reality often doesn’t match the perception.

Take, for example, this fascinating duo I wrote about: a $500K-a-year couple, both lawyers in their early 30s, raising two young kids in New York City. On paper, they’re living the dream. In reality, their budget tells a much more relatable tale of financial pressure, thanks to the crushing costs of big-city living.

The good news? With some strategic financial planning and the right tools, even households like this can break free from the rat race faster than they think.

Below is their infamous budget—yes, the one that went viral and made the finance internet collectively gasp. With a net worth of only about $350,000, including home equity and 401(k)s, they’re evidence that even the highest earners can face financial challenges. Let’s explore how they can turn things around.

A Typical $500K A Year Income Household Budget

After shelling out $185,600 in taxes, $42,000 for childcare and private school tuition, $87,500 for housing, and a laundry list of other expenses, this couple is left with a mere $600 at the end of the month. That’s hardly a buffer for surprise bills, let alone a safety net to build wealth or invest in their future dreams.

The shocking part? They’re essentially living paycheck-to-paycheck on half a million dollars a year. The stress of keeping up with high costs, coupled with the constant pressure to maintain appearances, leaves them wondering when—or if—they’ll ever be able to retire. Both are burning out working 60+ hours a week and hardly ever see their children.

Sound familiar? Plenty of dual-income families in major cities face the same challenges, but few are willing to speak up for fear of being judged. After all, how do you complain about “struggling” on $500K without someone telling you to check your privilege? But here’s the truth: the stress of not feeling financially secure isn’t exclusive to any income bracket—it’s something many of us grapple with.

Here’s a clear look at where this household’s $500,000 income is going and why it feels like it’s never enough.

Lessons From The $500K Budget Redo

When I first shared their budget, the internet erupted. Hundreds of comments poured in, with reactions ranging from disbelief to outright criticism. Some found their spending downright ridiculous, calling out their “champagne problems.” While only a small minority empathized with the challenges of raising a family in one of the priciest cities on earth.

But one thing stood out: their income wasn’t the issue. Earning half a million dollars a year is more than enough to thrive. The problem was how they managed it.

Taking the internet’s feedback as inspiration, I went back to the drawing board to see how they could optimize their cash flow without giving up the comforts they’d grown accustomed to. I made them cook more at home, sell and buy a cheaper house, do more of their home maintenance, get rid of their BMW, spend less on clothes and children’s lessons, pay less taxes by contributing to an HSA, and donate less to charity (sorry).

After crunching the numbers and fine-tuning their spending habits, they managed to free up $48,890 annually, boosting their total surplus to $56,190. Progress, indeed!

From Feeling Trapped Forever To Seeing The Light At The End Of The Tunnel

By trimming their annual expenses from $278,400 to $230,305, they also reduced their financial independence target. Instead of a daunting $6,960,000, their new goal—using the 25X rule—is $5,756,625. With a net worth of $350,000 and $56,190 a year in new investments, compounded at an 8% annual return, they could hit that target in 23 years.

Twenty-three years to freedom is a step up from feeling stuck in the rat race forever. But let’s be real—23 more years of grinding when you’re already teetering on burnout? That’s no dream life. To truly escape the hamster wheel, they need to think bolder and go even more aggressive.

Instead of planning to last 23 years and retire in their 50s, let’s figure out how they can hit the ideal retirement age even sooner. By addressing both short-term cash flow and long-term goals, we can build a plan to reshape their financial future with a more aggressive approach.

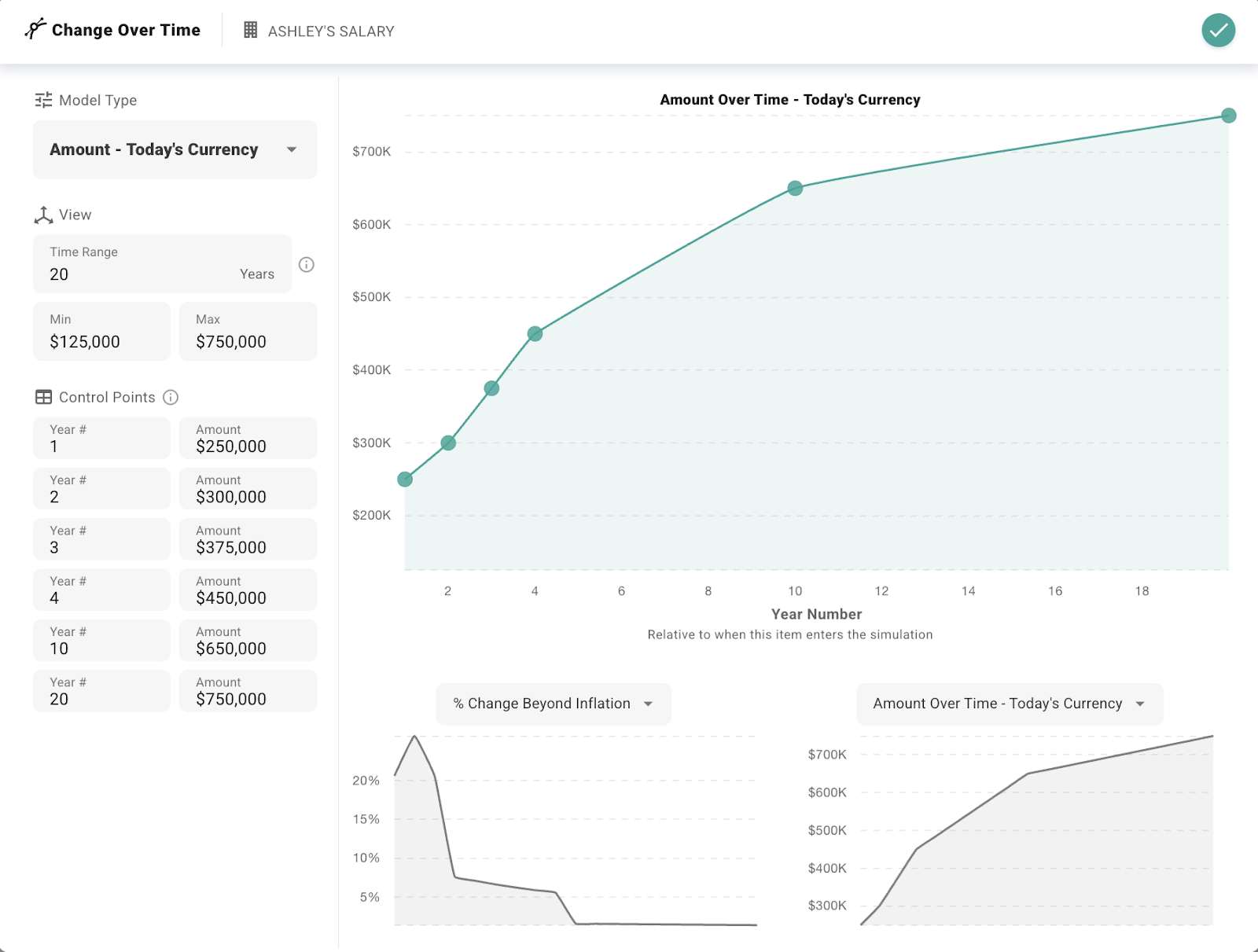

To help this couple escape the rat race and build a plan for financial freedom sooner, I decided to try something I’d been hearing more about: ProjectionLab. It’s a modern financial planning tool that seemed perfect for their situation. For anyone focused on financial independence, it’s worth exploring.

Optimizing Cash Flow Now

For many high earners, freeing up cash flow starts with targeting inefficiencies. Fully funding their 401(k)s and HSAs is a no-brainer—reducing taxable income while significantly boosting retirement savings. Making debt repayment a priority by adding $2,000 a month to student loans also clears debt faster and frees up future cash flow.

And by shifting from ride-sharing to public transit, while also cutting down miscellaneous expenses, they free up an extra $5,000 annually to invest in their financial goals. ProjectionLab makes your cash flow priorities easy to optimize.

Strategic Career Moves To Boost Income And Lifestyle

In addition to optimizing spending, increasing income and improving work-life balance can make a huge difference. A couple in their situation might consider:

One Spouse Intensely Focuses On Career Growth: One spouse could commit to the partner track at their firm, focusing on raises and bonuses that steadily increase earning potential. Sure, this spouse will see their kids even less, but that’s the sacrifice they need to make to earn even more than $500K/year. Equity partners at big law firms now make on average $1.4 million a year, but of course, not everybody can become one.

The Other Spouse Focuses on Work-Life Balance: One spouse might transition to an in-house counsel role at an established corporation or maybe a venture-backed startup. In-house counsel positions are typically less demanding since there’s only one client to serve and clearer objectives to follow. The median compensation for a general counsel in 2023 was $325,000, according to a detailed report by an in-house compensation survey report. This shift can help maintain a competitive salary while reducing work hours, providing greater flexibility for family responsibilities and potentially lowering childcare expenses.

If this lawyer couple in their early 30s can just keep climbing the corporate latter for another 10 years, they could see their household income grow far beyond $500,000 a year. Earning a total household compensation of $750,000 a year is a high probability. And if they can keep their expenses stable, their saving rate will go way up.

These strategies position them for consistent income growth while reducing the risk of burnout—a key consideration for high-pressure fields.

Relocate To A Lower-Cost Area To Save

Looking further ahead, a strategy like geo-arbitrage could better align their lifestyle with their long-term goals of early retirement. Selling their NYC condo and moving to a lower-cost state like New Hampshire could allow them to pay cash for a home, eliminate New York’s state and city income taxes, and save tens of thousands annually on housing.

Beyond the financial benefits, being closer to family and to children attending college nearby could reduce travel expenses and strengthen family connections.

Simplifying their lifestyle and aligning their spending with their values shaves an additional six years off their timeline to financial independence—putting them on track to retire comfortably in their mid-40s.

The Power of Visualization With ProjectionLab

Visualizing a financial plan isn’t just practical—it makes the process fun and exciting. Testing “what if” scenarios transforms financial planning from guessing to knowing which decisions have the greatest impact. It’s empowering to see how specific changes play out over time.

For example, comparing investing versus accelerating student loan payments forces you to weigh the financial benefits against the psychological value of freeing up cash flow. And let’s face it, paying off loans while saving for your kids college costs at the same time feels inefficient. Why not eliminate debt first and create more breathing room for the future?

Relocating to a lower-cost state like New Hampshire from New York isn’t just about cutting housing costs—it accelerates financial independence in ways that are hard to ignore.

Being able to map out a plan and see progress in real time provides clarity and confidence. When the temptation arises to splurge on a business-class upgrade or keep up with peers, having a visual representation of your goals helps you stay grounded. Revisiting the plan refocuses your priorities and reminds you what you’re working toward.

Using ProjectionLab, you can quickly map income, expenses, and savings goals to create a clear baseline and test adjustments—maxing out retirement accounts, prioritizing debt, making career moves, and exploring geo-arbitrage. Seeing the long-term impact of every decision makes the journey to financial independence not only achievable but something to look forward to.

Achieving financial independence isn’t just about earning and saving—it’s about having a clear strategy and a plan that aligns with your goals. Tools that let you visualize your financial choices and their impact create an essential roadmap for turning your actions into the life you want.

Revisiting the $500K a year couple’s finances with ProjectionLab highlighted just how powerful planning tools can be. Testing “what if” scenarios and seeing the trade-offs of their decisions in real time made it clear where they could take actionable steps toward financial independence.

Here’s what stood out about ProjectionLab and why it might be the tool for you:

Create and Compare Plans

Start by creating a clear picture of your financial situation. Enter your income, expenses, savings, and debt, and ProjectionLab will generate a baseline projection. This roadmap helps you identify opportunities and gaps, so you can make informed decisions and stay on track.

Test “What If” Scenarios

What happens if you accelerate debt repayment? Max out your 401(k)? Start a family? ProjectionLab makes it easy to test these scenarios side by side, so you can prioritize the changes that matter most.

Plan for Retirement

Simplify retirement planning by modeling tax-efficient withdrawal strategies, accounting for inflation and healthcare costs, and determining the earliest age you can retire while maintaining your desired lifestyle.

Adapt in Real Time

Life changes, and so should your financial plan. ProjectionLab allows you to update projections instantly, keeping your roadmap actionable and aligned with your goals.

Keep Your Finances on Track

Understanding where your money goes and tracking progress toward milestones are critical for financial success. ProjectionLab breaks down your cash flow and expenses into detailed projections and helps you set and monitor financial goals. Whether you’re saving for a home or aiming for early retirement, the tool helps you stay on track or adjust as needed.

Stress-Test your Plan

Uncertainty is an unavoidable part of financial planning. Using Monte Carlo simulations, ProjectionLab evaluates your financial plan under different market conditions, providing a probability of success. This feature helps you make decisions grounded in data, even when the future feels unpredictable.

Optimize Taxes

Smart tax planning can have a huge impact on your long-term wealth. ProjectionLab helps you analyze Roth conversions, evaluate tax-advantaged accounts, and maximize your tax efficiency over time.

A Financial Tool For Everyone

ProjectionLab isn’t just for high-income earners. It’s for anyone who wants clarity and confidence in their financial decisions, no matter where you’re starting from. Whether you’re exploring early retirement, questioning renting vs buying, or planning other major milestones, ProjectionLab empowers you to visualize your options, test strategies, and build a future you can feel good about.

It’s great to have options. Having reviewed tools like Boldin and Empower, each brings its own strengths. Where ProjectionLab stands out is in full-life financial planning with great visualizations. The ability to test and compare detailed scenarios make it a powerful tool for turning goals into actionable plans. You’ll also be able to understand how every decision impacts your path to financial freedom.

Take Control Of Your Finances Today

Imagine if small changes to your own spending could help you shave years off your retirement timeline. With just a few smart adjustments, you too can reduce the amount you need to retire earlier.

Ready to turn your goals into reality? Financial independence starts with a plan. Build your personalized roadmap with ProjectionLab today and take the first step toward freedom. You can try it for free!

ProjectionLab is a new affiliate partner of Financial Samurai. I’m constantly testing the best financial products available to help readers better manage their finances and grow their wealth.

To expedite your journey to financial freedom, join over 60,000 others and subscribe to the free Financial Samurai newsletter. Financial Samurai is among the largest independently-owned personal finance websites, established in 2009. Everything is written based on firsthand experience and expertise.